Vietnam’s e-commerce market is growing at an impressive pace and is expected to surpass USD 30 billion by 2026. With a young, digitally native population, high internet penetration, and the explosive rise of platforms such as Shopee, Lazada, and TikTok Shop, this is an ideal time for foreign investors to establish an e-commerce business in Vietnam.

Moreover, the Law on Investment 2025 (effective March 1, 2026) and the Law on Electronic Commerce 2025 have introduced significant reforms. These changes make it much easier for foreign investors to own 100% of their company and operate fully online businesses in Vietnam.

This article offers a clear, step-by-step guide on how to set up an e-commerce business in Vietnam in 2026 – from choosing the right business model to full operational launch. It is specially designed for foreign investors interested in establishing an online trading company in Vietnam.

1. Vietnam E-Commerce market outlook 2026 & promising sectors

Vietnam’s e-commerce sector is becoming increasingly diverse, with strong potential across multiple industries – particularly attractive for FDI investors.

Key promising sectors include:

- Fashion & Beauty: High demand, fast inventory turnover, and excellent scalability through social commerce.

- Electronics & Technology: Strong profit margins and well-suited for cross-border models.

- Health & Wellness: Significant post-COVID growth, especially in functional and nutritional products.

- Home & Living: Benefiting from long-term shifts in online shopping habits.

- Food & Beverages (especially fresh products): High potential, although it requires robust logistics.

- Imported Products (cross-border): Leverages the appeal of international brands.

- Eco-friendly & Sustainable Products: An emerging trend, particularly popular among younger consumers.

What these sectors share is rapidly growing demand, easy access to online customers, and strong potential for foreign companies to scale successfully.

2. Step 1: Step 1: Choose the Right Model to Set Up an E-Commerce Business in Vietnam

Before taking any concrete steps, clearly defining your overall business model is the single most important decision when learning how to start an import-export business in Vietnam.

E-commerce is merely a sales channel, not the business model itself. You must first decide how your company will operate, whether through wholesale, retail, direct export, import and distribution, or a combination of several models.

The most common business models currently used by foreign investors in Vietnam include:

- Wholesale (B2B): Importing goods in large volumes and selling them to retailers or other businesses. This model is ideal for companies focused on supply chain efficiency and high-volume transactions.

- Retail (B2C): Selling products directly to end consumers, either through physical stores or online channels.

- Direct Export: Focusing on exporting Vietnamese-made products to international markets.

- Import and Distribution: Importing goods from overseas and distributing them within Vietnam (this can combine both wholesale and retail activities).

- Hybrid Model: Combining multiple approaches (for example, wholesale + online retail + export) to maximize revenue streams and flexibility.

E-commerce can be applied to any of the above models, whether through your own website, selling on major marketplaces such as Shopee, Lazada, or TikTok Shop, or using a combination of online and offline channels.

Practical Recommendation

Many foreign investors begin with an Import and Distribution model combined with a Hybrid approach (wholesale + online retail). This allows them to test the market and validate demand before making larger investments. Clearly defining your business model early on will help you choose the right company structure, prepare the correct licenses, and avoid costly adjustments later in the process.

3. Step 2: Company Registration (FDI Setup)

To legally set up an e-commerce business in Vietnam, foreign investors must first establish a compliant legal entity. The most common and flexible choice is a 100% foreign-owned Limited Liability Company (FDI LLC).

The standard registration process includes:

- Obtaining the Investment Registration Certificate (IRC)

- Obtaining the Enterprise Registration Certificate (ERC)

Under the Law on Investment 2025, in many non-restricted sectors, investors can now apply for the ERC first and complete the IRC later – significantly shortening the overall setup timeline.

Once the licenses are granted, the company must:

- Open an investment bank account

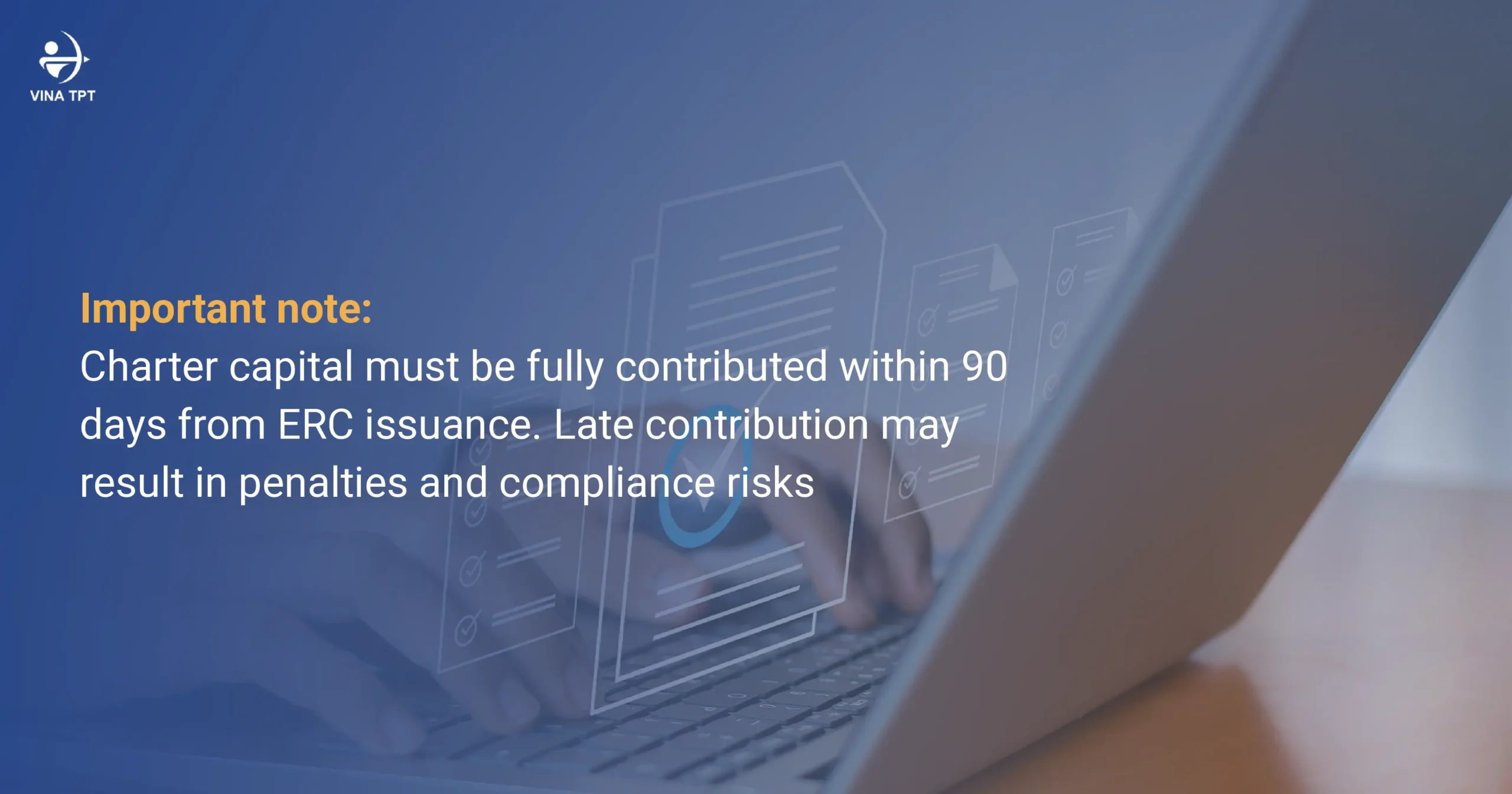

- Contribute charter capital within 90 days

- Register the company seal and tax code

With complete and accurate documentation, the entire process usually takes 6 to 8 weeks.

Explore Company Formation Services & Get Free Consultation

4. Step 3: Obtain E-Commerce Operating License

After company registration, businesses must fulfill specific licensing requirements for e-commerce activities.

Companies are required to register or notify their e-commerce operations with the Ministry of Industry and Trade, depending on the chosen model. For platforms with foreign elements, appointing a Local Authorized Representative in Vietnam is often mandatory.

Additional operational requirements typically include:

- Seller verification systems (VNeID)

- Clear complaint handling policies

- Robust personal data protection mechanisms

If the business sells regulated products such as food, cosmetics, or medical devices, additional specialized licenses will be required.

5. Step 4: Setup Operations & Compliance

Once all legal formalities are completed, the focus shifts to building efficient day-to-day operations. Key areas to address include:

- Payment systems: Open corporate bank accounts and integrate local and international payment gateways.

- Logistics & warehousing: Partner with reliable providers such as SPX or J&T, or develop your own network.

- Human resources: Recruit staff and ensure full compliance with labor regulations, including work permits for expatriates where necessary.

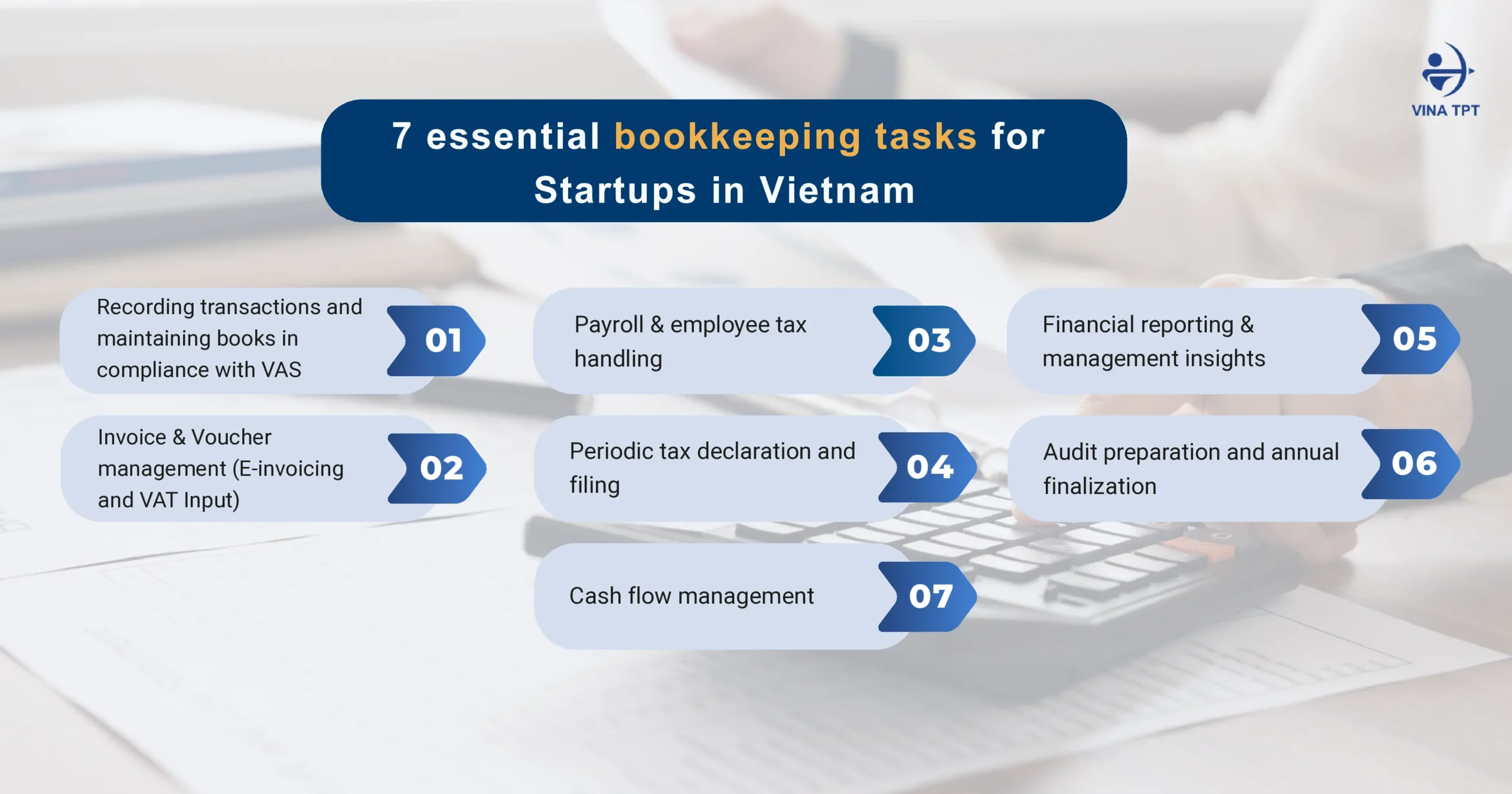

- Accounting & tax: Establish a VAS-compliant accounting system, manage VAT, and handle electronic invoicing correctly.

Setting up these elements correctly from the beginning helps avoid costly mistakes and ensures smooth, scalable operations in the long term.

6. Common Challenges When You Set Up an E-Commerce Business in Vietnam

Although Vietnam’s e-commerce market is growing rapidly and offers tremendous potential, setting up and operating an online business in the country still presents foreign investors with a number of practical challenges. If not properly anticipated, these difficulties can delay project timelines, increase operating costs, and even undermine long-term competitiveness.

One of the biggest hurdles is the strict requirement for legal presence and regulatory compliance. Foreign investors must not only establish an FDI company but also register their e-commerce activities with the Ministry of Industry and Trade, appoint a Local Authorized Representative in Vietnam, and implement robust personal data protection mechanisms in line with the Law on Cybersecurity and the Law on Personal Data Protection. Any misstep in this process can lead to heavy administrative fines or even suspension of operations.

A second major challenge is the intense competition from dominant local platforms. Shopee, Lazada, TikTok Shop, and other established domestic marketplaces already control the majority of the market share with powerful promotional campaigns, massive user bases, and ready-made infrastructure. Building brand awareness, attracting new customers, and competing on price requires a smart marketing strategy and a substantial budget.

Third, logistics and supply chain limitations remain a significant obstacle. Although the sector has developed quickly in recent years, service quality still varies considerably across different regions. Deliveries to remote and rural areas are often slower, have lower success rates, and incur higher costs – all of which directly impact customer experience and profitability.

To successfully navigate these challenges, businesses need a clear strategy from the outset, strong partnerships with reputable local players, and professional FDI consulting support. Working with experienced advisors helps minimize risks, optimize costs, and accelerate operational readiness.

7. Why Vina TPT Can Help You Set Up Your E-Commerce Business

Vina TPT offers a comprehensive, end-to-end solution to help foreign investors successfully set up an e-commerce business in Vietnam.

We provide full support from company formation and e-commerce licensing to the establishment of accounting, tax, and payroll systems. Drawing on extensive experience working with FDI companies, Vina TPT ensures you not only comply with all legal requirements but also launch operations efficiently and effectively from the very first day.

Contact Vina TPT today if you plan to set up an e-commerce business in Vietnam with full legal and operational support.