For foreign investors entering the Vietnamese market, tax compliance is not simply an obligation to pay taxes to the state budget, but a critical factor that directly impacts the financial safety and long-term sustainability of the investment project. Language barriers, the complexity of the local legal system, and the frequent updates to sub-law documents often turn tax management into the biggest “bottleneck” for FDI company management.

Even a small mistake in identifying invalid invoices, incorrectly posting non-deductible expenses, or late declaration of contractor taxes can result in heavy administrative fines, additional tax assessments with 0.03% daily late payment interest, or prolonged tax inspections that disrupt the entire supply chain.

This article provides a comprehensive overview of tax compliance Vietnam FDI, an in-depth analysis of the four core taxes (VAT, CIT, PIT, FCT) with the latest legal obligations, and reveals Vina TPT’s specialized Vietnam tax obligations for foreign companies solutions to help investors take full control of their financial game in Vietnam.

1. Value-Added Tax (VAT) – The Most Important Tax Obligation for all Businesses

Value-Added Tax (VAT) is an indirect tax with the highest transaction frequency and the strictest supervision from local tax authorities. It is a mandatory obligation applicable to all business sectors of FDI companies in Vietnam, including trading, manufacturing, services, import-export, and other fields.

1.1. Legal Basis & Declaration Cycle

According to the Law on Value-Added Tax 2008 (as amended and supplemented) and the latest guidance in Decree 181/2025/ND-CP, newly established FDI enterprises or those with annual revenue of VND 50 billion or less in the previous year must declare VAT on a quarterly basis. Enterprises with previous year revenue exceeding VND 50 billion are required to declare VAT on a monthly basis.

1.2. Strict Conditions for Input VAT Deduction

To be eligible for input VAT deduction, the accounting department of an FDI company must simultaneously meet the following conditions:

- Have a valid VAT invoice (issued with a tax authority code under Decree 123/2020/ND-CP).

- Have non-cash payment documents (bank transfer from the buyer’s account to the seller’s account) for invoices valued at VND 5 million or more (including VAT).

- The purchased goods or services must be directly used for the production or business of goods and services subject to VAT.

2. Corporate Income Tax (CIT) – Profit-Based Tax & the Provisional Payment Calculation

Corporate Income Tax (CIT) directly affects the net profit of foreign investors. Understanding the provisional payment rules and tax incentive mechanisms is the key to optimizing capital efficiency.

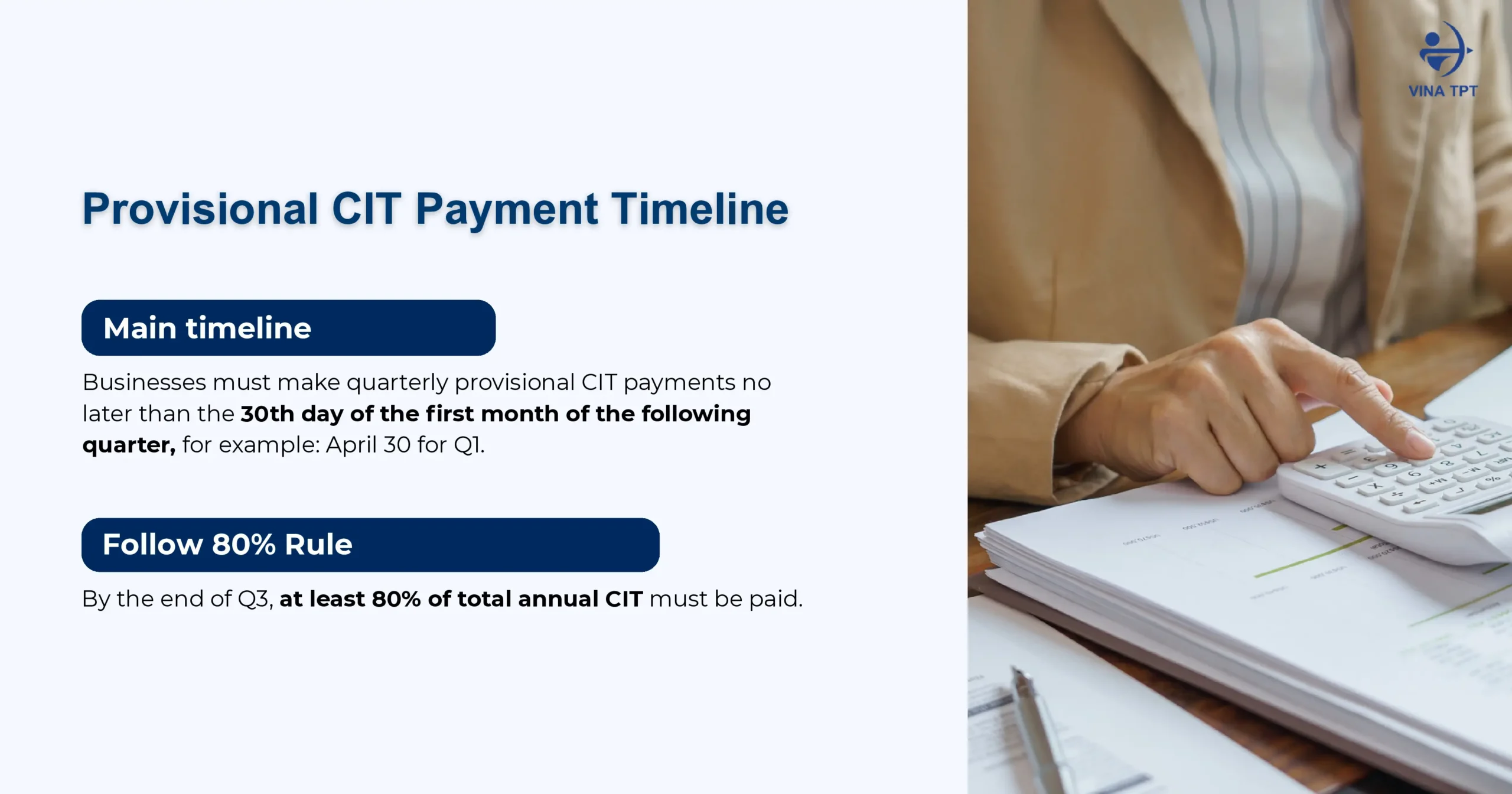

2.1. Standard Tax Rate & Quarterly Provisional Payment Rule (80% Rule)

The standard Corporate Income Tax (CIT) rate in Vietnam is currently 20% on taxable income. However, according to the new regulations in 2025, certain enterprises that meet the preferential conditions may enjoy lower tax rates:

- 15%: Applied to enterprises with annual total revenue not exceeding VND 3 billion.

- 17%: Applied to enterprises with annual total revenue from over VND 3 billion up to VND 50 billion.

Special Note on the 80% Rule:

Special Note on the 80% Rule: According to current regulations, the total CIT amount provisionally paid for the four quarters of the tax year must not be less than 80% of the final CIT amount payable upon annual finalization. If the payment falls short of this 80% threshold, the company will be charged late payment interest (0.03% per day) on the shortfall, starting from the day after the deadline for the fourth-quarter tax payment.

2.2. Tax Incentive Mechanism (Tax Incentives) under the Law on Investment 2020

FDI companies can take advantage of attractive tax incentive packages if they meet the conditions regarding location or investment priority sectors according to Decree 31/2021/ND-CP:

|

Type of Incentive |

Incentive Level |

Conditions & Applicable Sectors |

| Preferential tax rate of 10% | For 15 years (extendable to 30 years) | High-tech projects, high-tech applications, R&D, renewable energy. |

| 100% Exemption & 50% Reduction | Exemption for 4 years, 50% reduction for the next 9 years | Newly established projects in industrial parks, economic zones, or areas with particularly difficult socio-economic conditions. |

| Preferential tax rate of 15%–17% | Applied throughout the project duration | Enterprises meeting capital scale or large labor usage criteria as prescribed. |

Key updates in 2025:

- Enterprises are allowed to expand deductible expenses related to scientific research, digital transformation, new technology testing, emission reduction, and community activities.

- If eligible for multiple incentive groups, the enterprise has the right to choose the most favorable incentive level.

- Losses can be carried forward continuously for a maximum of 5 years, and up to 20% of taxable income may be set aside to establish a Science & Technology Development Fund (if used for the correct purposes).

Real-life example: A Korean technology corporation established a software factory in Ho Chi Minh City High-Tech Park. By correctly applying for CIT incentives, the company enjoys a 10% tax rate for 15 years, 100% CIT exemption for the first 4 years (from the year it has taxable income), and a 50% reduction for the next 9 years – saving millions of USD in taxes.

>>> For a more detailed and complete update on all Corporate Income Tax incentive policies in 2025, read the article: Tax Incentive in Vietnam 2025: Comprehensive Guide to Optimize Profits under New CIT Law

Get Expert Advice on Tax Incentive Policies

3. Personal Income Tax (PIT) and Social Insurance Responsibilities for Personnel

Compliance with Personal Income Tax (PIT) and Social Insurance (BHXH) for the workforce – especially for foreign experts and managers (Expats) – always carries significant risks of additional tax assessments if residency status is not correctly classified.

3.1. PIT Withholding & Residency Classification Rules

FDI companies are obligated to withhold, declare, and pay Personal Income Tax (PIT) on a monthly or quarterly basis before paying income to employees:

- Resident Individuals: Present in Vietnam for 183 days or more in a calendar year (or 12 consecutive months). Progressive tax rates from 5% to 35% apply on worldwide income (Global Income).

- Non-Resident Individuals: A non-resident individual is a person who does not meet the conditions of a resident individual, specifically someone who is present in Vietnam for fewer than 183 days in the tax year and does not have a permanent residence in Vietnam.

3.2. Mandatory Social Insurance (BHXH) Responsibilities

According to the Law on Social Insurance and related regulations, FDI companies must contribute the following for employees:

- Vietnamese Employees: Contributions to Social Insurance, Health Insurance, and Unemployment Insurance at a total rate of 32% (Employer: 21.5%, Employee: 10.5%).

- Foreign Employees (Expats): Mandatory participation in Social Insurance and Health Insurance if they hold a Work Permit and have an employment contract that is indefinite or has a term of 1 year or longer.

>>> For more details:

- Personal Income Tax 2026: Key Changes Directly Affecting Employees

- Vietnam Tax Handbook for investor of Vina TPT

4. Foreign Contractor Tax (FCT) and Related Legal Obligations

Foreign Contractor Tax (FCT) is a special tax that many newly operating FDI companies often overlook, leading to declaration violations and penalties.

4.1. Nature & Mechanism of FCT Collection

FCT applies to foreign organizations and individuals who do not operate under Vietnamese law but generate income from providing services or goods associated with services in Vietnam (such as software royalties, parent company management consulting fees, cross-border digital marketing services, etc.).

FCT consists of two main components: VAT and Corporate Income Tax (or Personal Income Tax). The FDI company in Vietnam is responsible for withholding, declaring, and paying FCT on behalf of the foreign contractor before remitting payment.

Example: An FDI company pays USD 100,000 in software royalty fees to its parent company in Singapore. The company must determine the applicable FCT rate (typically 5% CIT on royalties), register a contractor tax code, and declare and pay FCT within 10 days from the payment date.

4.2. 2. Other Mandatory Fees & Periodic Reporting Obligations

In addition to the four main taxes, Vietnam tax obligations for foreign companies also include the Investment Activity Report (IAR): Periodic declaration and reporting of project implementation status on the National Investment Information System.

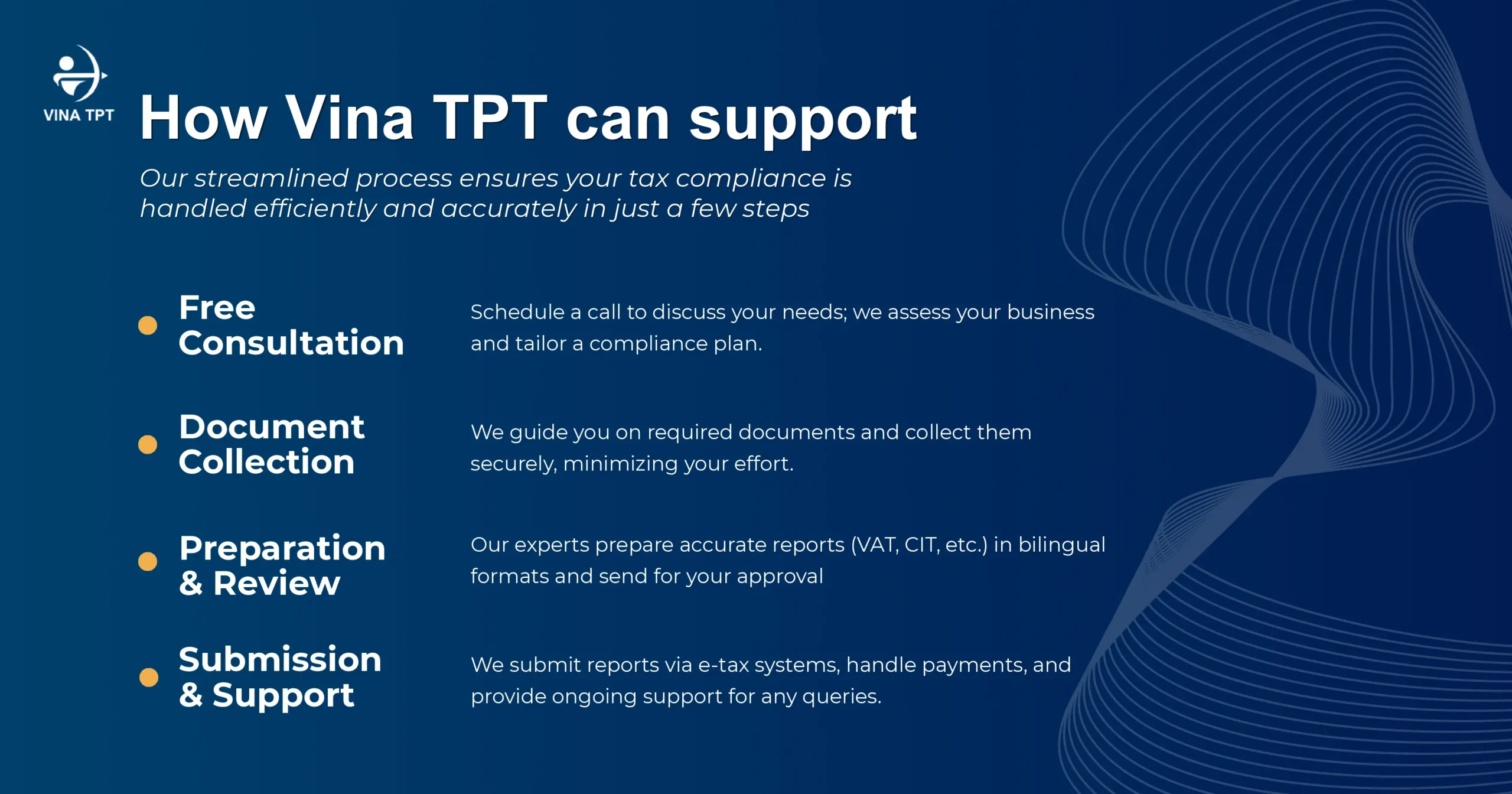

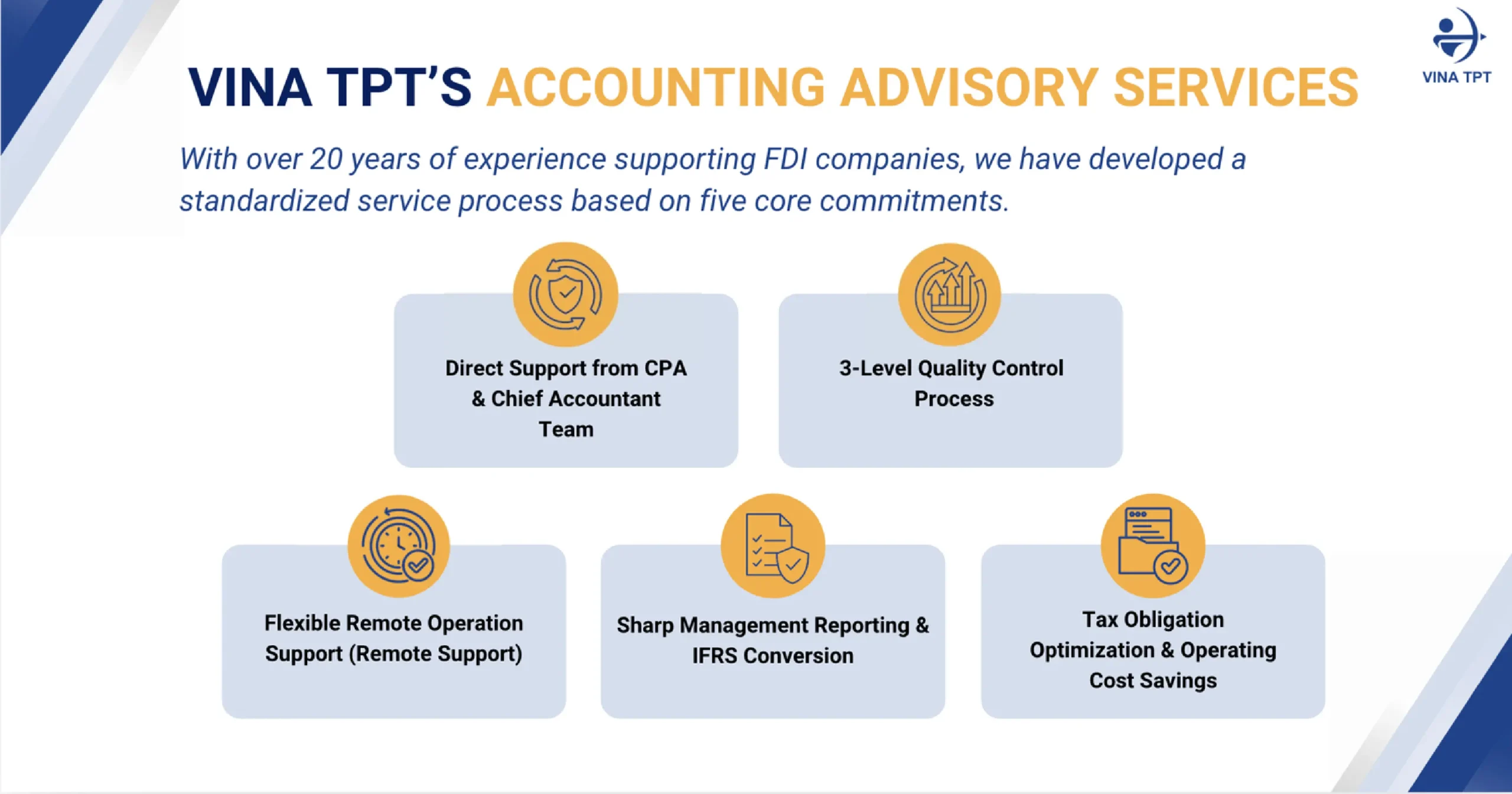

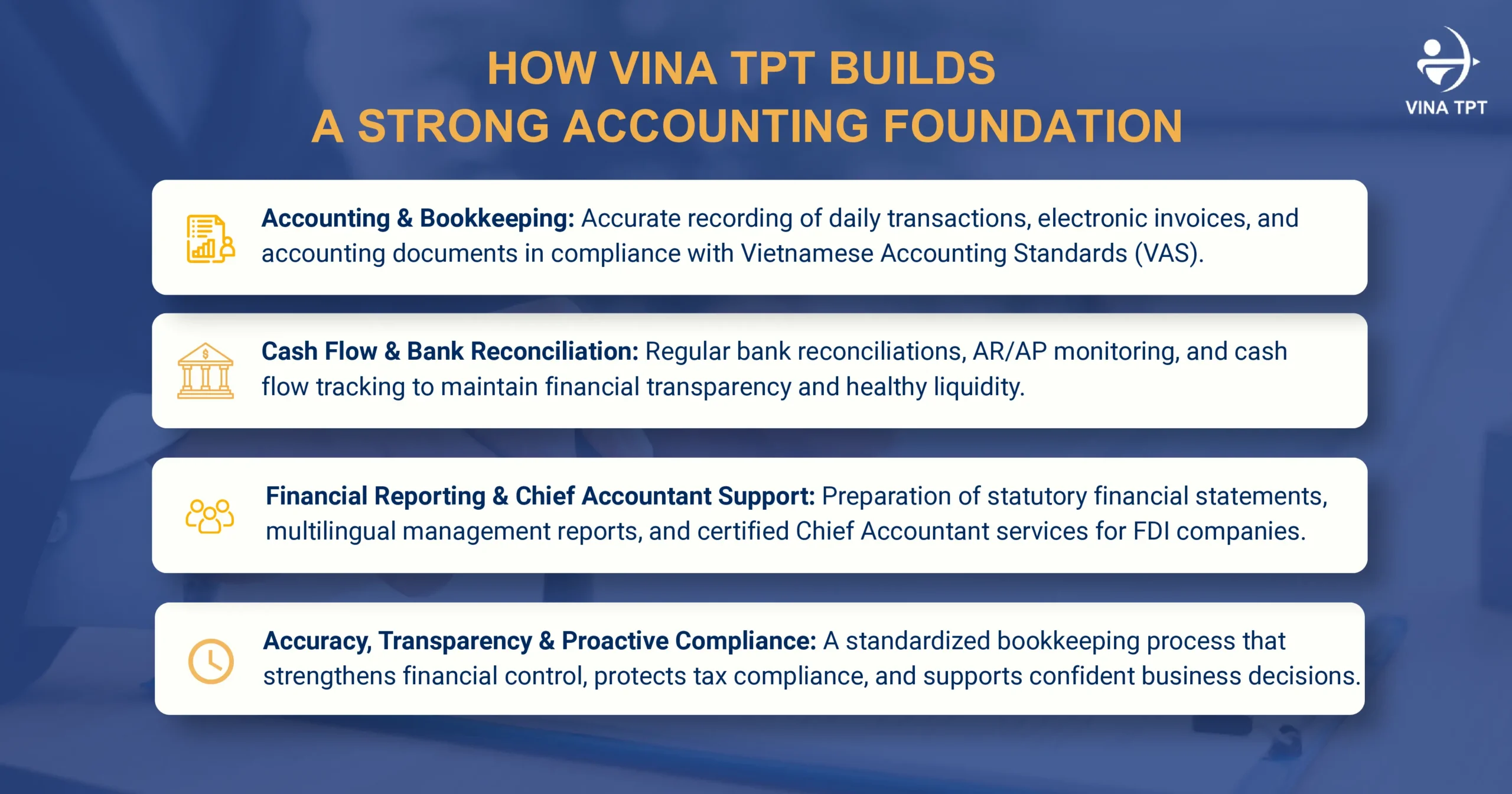

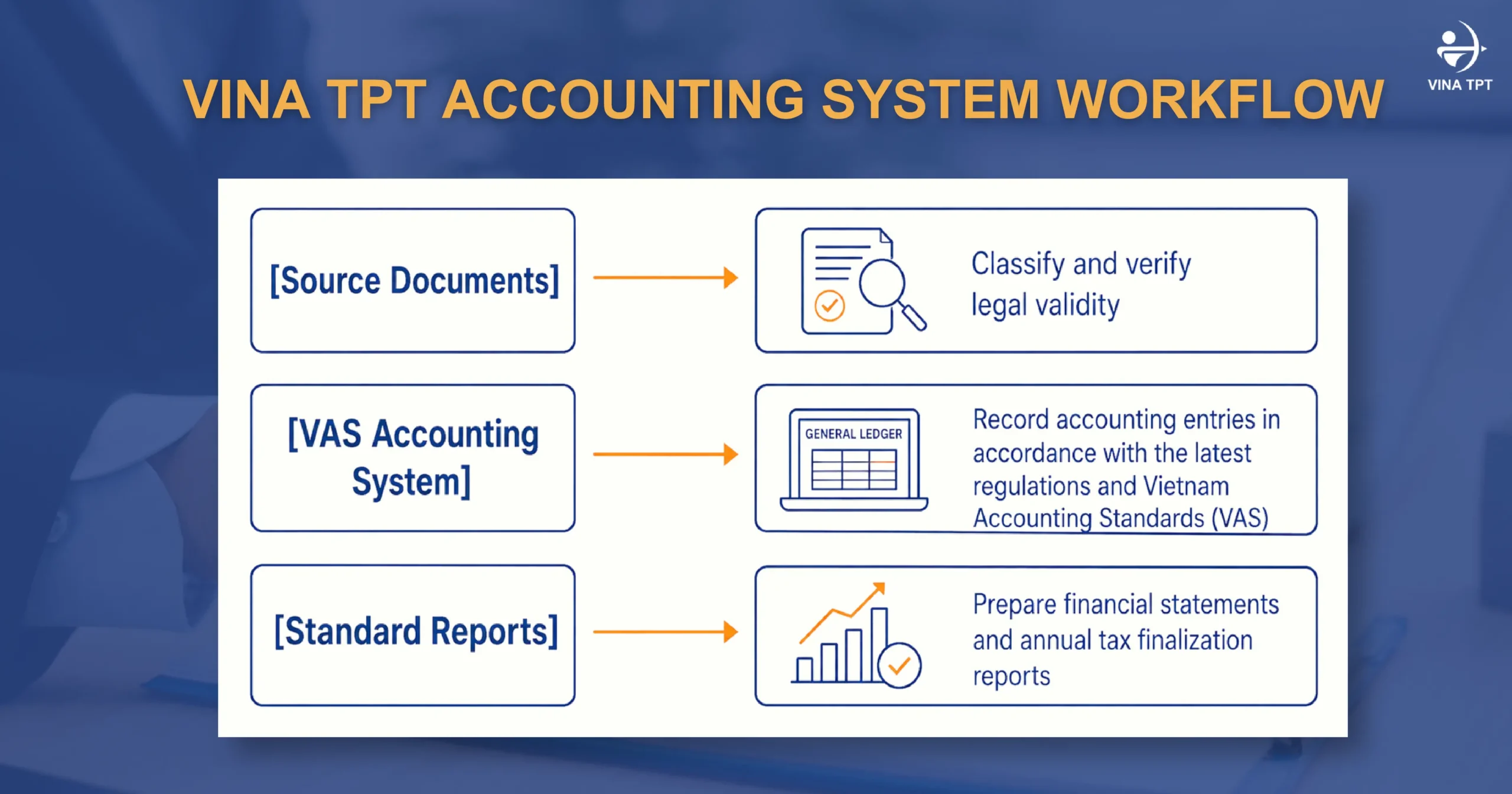

5. Benefits of Using Vina TPT’s Tax Compliance Services

When choosing to partner with Vina TPT, FDI companies are not simply using an external tax filing service – they are proactively equipping themselves with a solid “financial shield” for the entire operational process in Vietnam.

Instead of maintaining a bulky in-house accounting and tax team with high costs while still facing risks of staff turnover or lack of legal update capabilities, partnering with Vina TPT helps businesses optimize operating costs by up to 40%. More importantly, thanks to a 3-level independent quality control model operated by experienced CPA and Chief Accountant experts, all risks of additional tax assessments, administrative penalties, or errors during finalization are eliminated at the root.

In addition to legal safety, Vina TPT acts as a strategic advisor, helping businesses legally maximize tax incentives and optimize deductible expense structures in line with the spirit of the Corporate Income Tax Law. At the same time, all financial data is standardized into bilingual management reports (English & Vietnamese), creating a transparent information bridge that allows the Board of Directors and overseas Headquarters to easily grasp the accurate financial picture in real time. All of this brings complete peace of mind, allowing foreign investors to focus entirely on market expansion goals.

Are you concerned about tax compliance? Contact Vina TPT today to receive a free consultation and specialized tax compliance services.