Many FDI companies, when first establishing operations in Vietnam, often ask: “Our team only has a few dozen people, or even fewer than 10 employees – do we really need to hire an external Vietnam payroll provider?” This is a completely practical concern as foreign investors seek to optimize their operating structure in the early stages of entering a new market. They often tend to have staff handle multiple roles or assign an internal accountant to manage everything from corporate accounting to payroll.

However, Vietnam’s legal environment and labor policies have very distinct characteristics and evolve continuously. Regardless of whether a company is small or large, the legal obligations related to salary calculation, contributions to Social Insurance, Health Insurance,, Unemployment Insurance, and Personal Income Tax (PIT) withholding are strictly monitored by the authorities. Even a small systemic error in declarations, delays in insurance contributions, or mistakes in applying progressive tax rates for expatriate employees can lead to heavy administrative fines, prolonged labor disputes, or serious damage to the company’s reputation with local government agencies.

So what exactly does a professional Vietnam payroll provider do to protect businesses from these risks? And is outsourcing this service truly worth the economic value for FDI companies? This article will analyze each aspect in detail, break down the specialized tasks of the service provider, and share how a professional Vietnam payroll provider like Vina TPT helps foreign businesses optimize operations.

1. What Services Does a Vietnam Payroll Provider Offer?

A reputable Vietnam payroll provider is far more than just a unit that inputs data into a computer and generates monthly payroll reports. In reality, they act as a professional HR and payroll department, taking full responsibility for the complex operational processes and ensuring tight alignment between your company’s internal policies and current legal regulations.

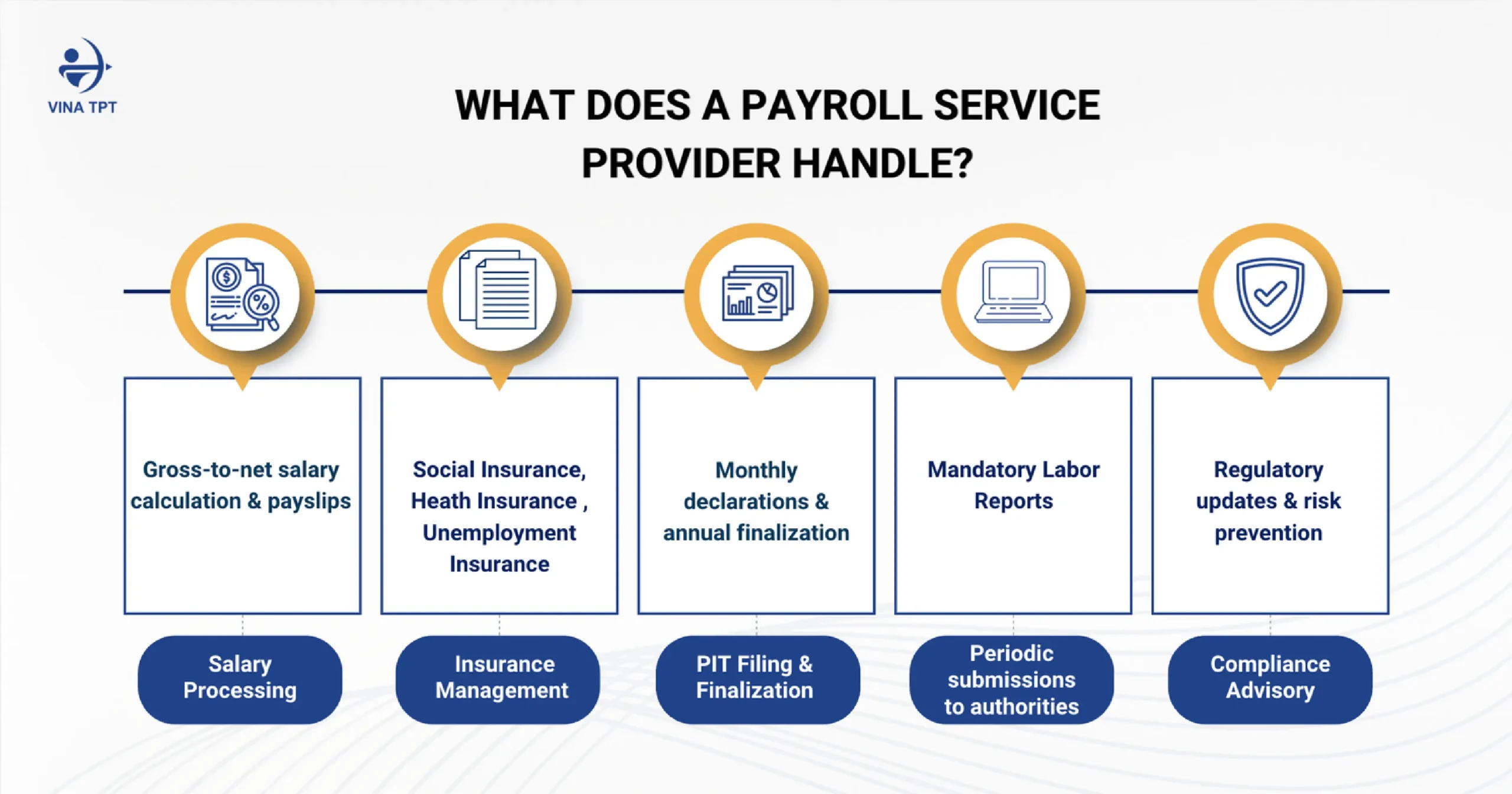

Specifically, the comprehensive service scope of a professional payroll provider in Vietnam includes the following core components:

- Accurate Salary Calculation and Secure Payslip Distribution: Precise calculation from gross to net salary, detailed allocation of tax-exempt allowances (meals, phone, uniforms), performance bonuses, and issuance of secure electronic payslips (Payslip) to each employee.

- PIT Compliance and Representation: Direct withholding of Personal Income Tax (PIT) from source, preparation of quarterly tax declarations, registration of new individual tax codes, registration of dependents, and handling of year-end PIT finalization on behalf of the company and employees.

- Full Management of Mandatory Insurance: Processing employee additions and terminations on the electronic social insurance system, closing social insurance books for departing staff, and directly handling benefit claims from the insurance fund (maternity, convalescence, sickness).

- Completion of Periodic Labor Reports: Preparing, standardizing data, and submitting all required reports on labor changes and occupational safety & health to the Ministry of Home Affairs (MOHA) according to the legally mandated deadlines.

2. Is Payroll Outsourcing Worth It for Your FDI Business?

Choosing the right payroll provider Vietnam businesses can rely on is often more cost-effective than building an in-house team. For FDI companies investing in Vietnam, the outsourcing model delivers clear strategic value and significant economic benefits:

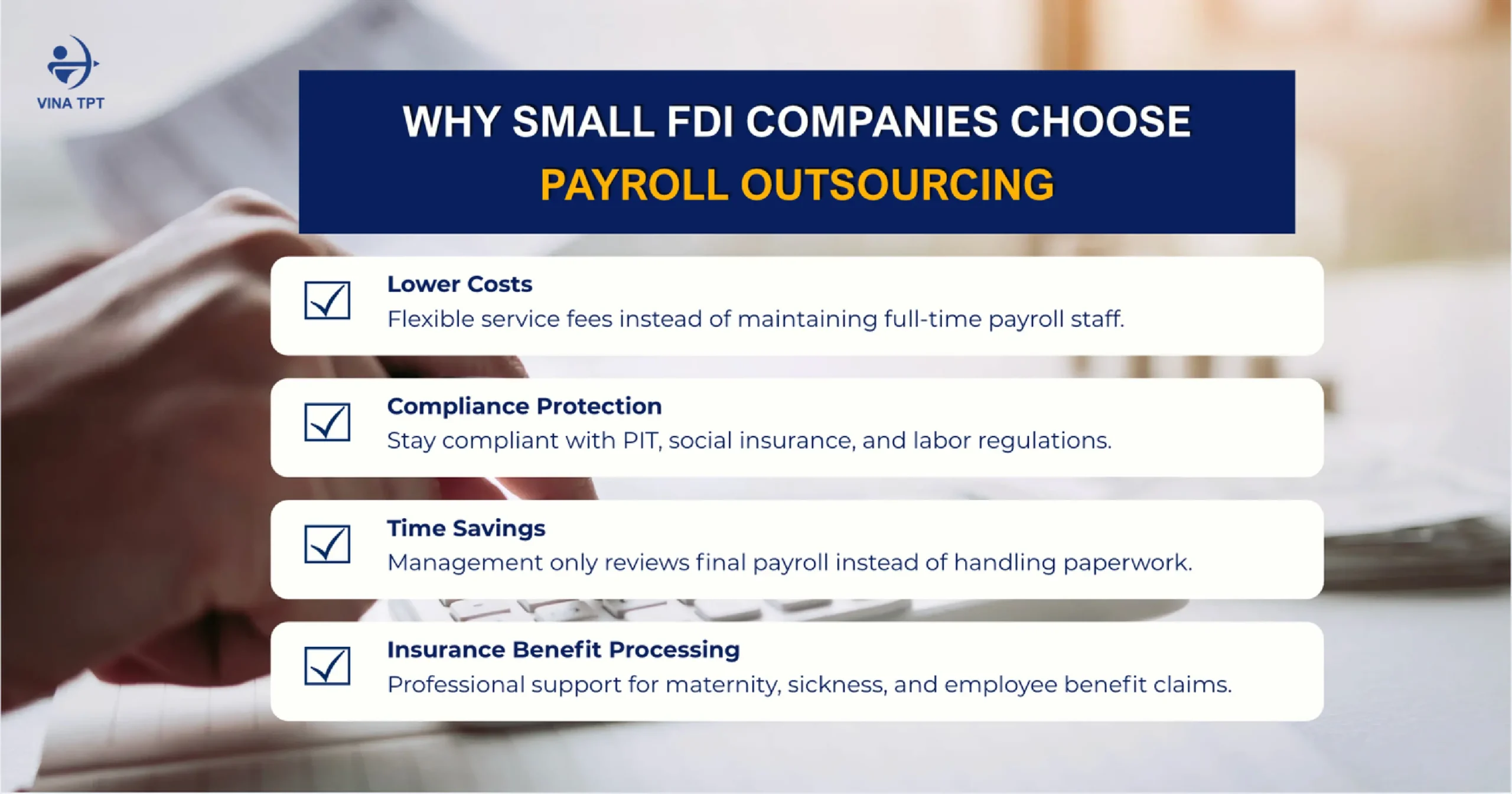

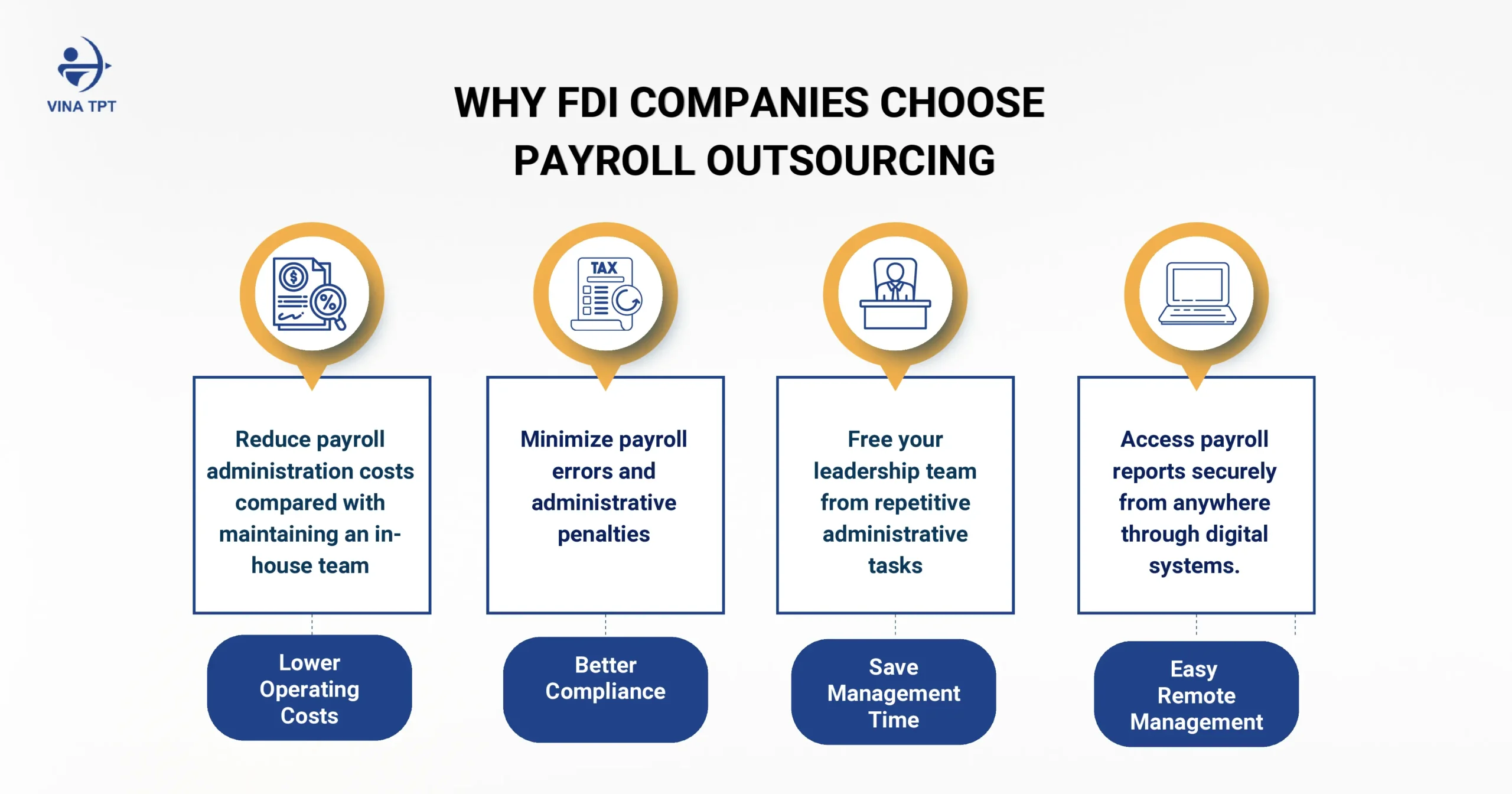

- Maximum operating cost savings: According to economic surveys, using outsourced services can help businesses reduce costs by 30-40% compared to maintaining an in-house payroll team. Internal costs go beyond base salaries and include recruitment, specialized training, insurance contributions, holiday bonuses, expensive dedicated payroll software licenses, and office space. With outsourcing, you only pay a fee based on the actual number of employees each month.

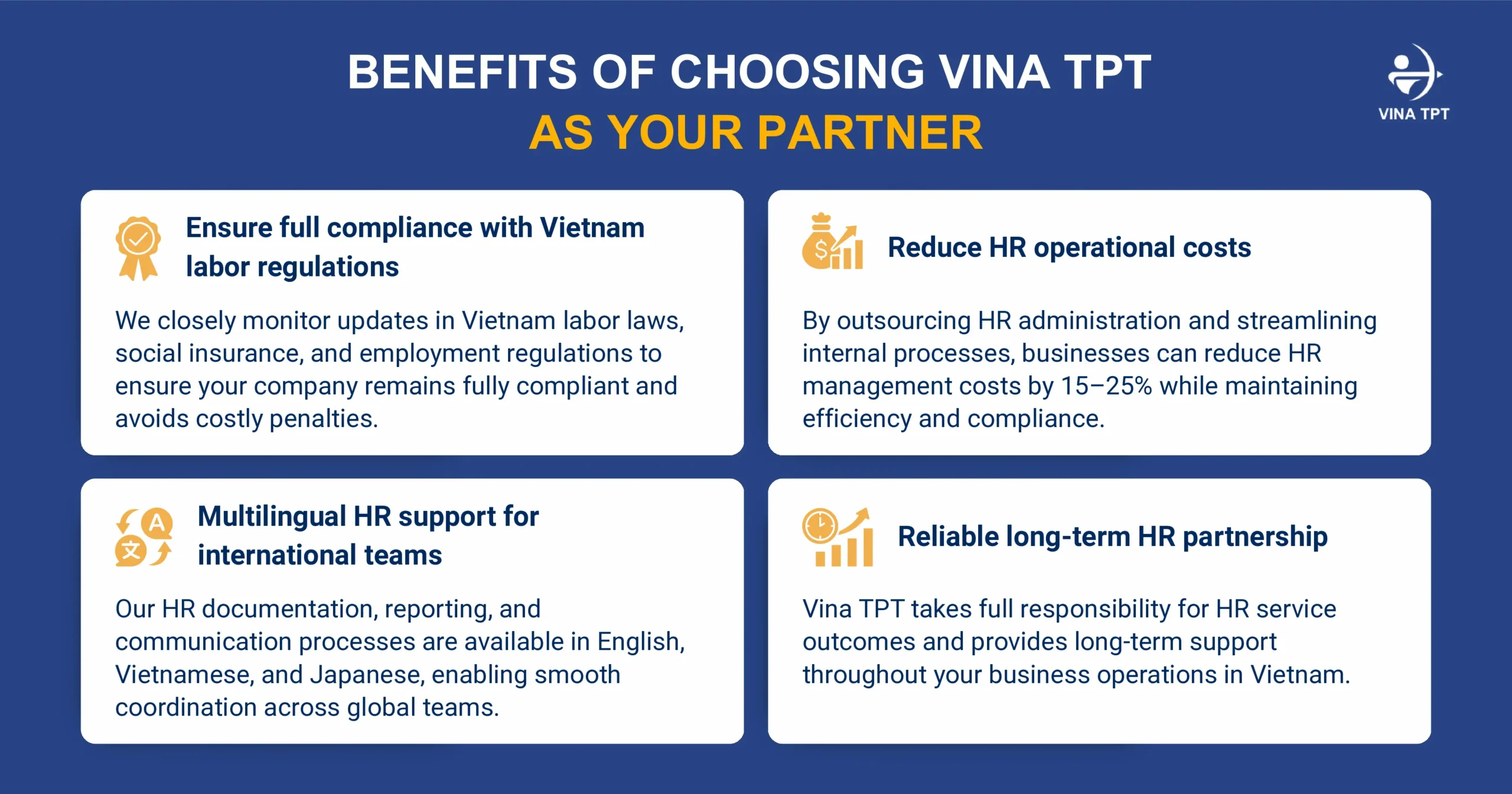

- Minimizing errors and administrative penalties: Labor, salary, and tax regulations in Vietnam are frequently updated with new decrees and circulars. If internal staff lack expertise or fail to stay current, errors in salary calculations, applying incorrect regional minimum wages, or wrong insurance contribution rates can easily occur. Professional payroll services providers have deep specialized knowledge and rigorous cross-checking processes, committing to take responsibility for technical errors and protecting your business from unnecessary labor disputes.

- Guaranteed full legal compliance: All systemic policy changes (such as adjustments to the base salary, dependent deductions for PIT, or new regulations on social insurance for foreigners) are immediately incorporated into the service provider’s calculation system. This ensures your FDI company always operates in full legal compliance in Vietnam without having to spend time researching legal documents yourself.

- Freeing up valuable management time: Instead of spending many hours each month approving documents, reconciling insurance data, or addressing minor employee questions about payslips, directors and FDI managers can devote 100% of their time and focus to core revenue-generating activities (core business) – such as product development, customer acquisition, supply chain expansion, and business strategy building.

- Maximum remote and flexible management support: The provider’s digitized payroll reporting and e-payslip system allows investors and overseas headquarters to easily monitor and approve labor costs remotely through secure online portals, eliminating geographical and time-zone barriers.

3. When Should FDI Companies Consider Outsourcing?

- Small to medium-sized businesses (3 to 20 employees): At this scale, hiring dedicated Compensation & Benefits (C&B) specialist is extremely wasteful, while a general accountant usually lacks deep expertise in complex insurance procedures and specific labor policies.

- Companies employing foreign staff (expats): The process of global PIT calculation, preparing documents for tax exemptions under Double Tax Avoidance Agreements, and handling social insurance contributions for expats requires very high legal expertise that only experienced professionals can manage smoothly.

- Businesses prioritizing leanness and confidentiality: Companies that want to minimize administrative and back-office functions to focus entirely on market expansion, while maintaining absolute confidentiality of salary information among internal positions (to prevent internal salary leaks that could harm team cohesion).

Explore Vina TPT Payroll Services

4. Common Concerns When Choosing a Vietnam Payroll Provider

When selecting a Vietnam payroll provider, foreign investors often have several important questions. Below are the most common concerns and practical answers from an expert perspective:

4.1. Is the service expensive, and how is the fee calculated?

In reality, outsourcing is much more cost-effective than maintaining an in-house team. Service fees are usually calculated flexibly based on the actual number of employees (per headcount) each month. A reputable provider will present a transparent pricing table from the beginning and commit to no hidden fees throughout the service period.

4.2. Are salary data and employee information safe?

This is a top concern for businesses. Professional service providers are required to use high-security certified digital platforms, encrypted cloud storage systems, sign strict non-disclosure agreements (NDA), and fully comply with Vietnam’s Cybersecurity Law and Personal Data Protection Decree (PDPD).

4.3. Does the service provider truly have deep expertise in labor law and related tax regulations?

Evaluate their capability through their track record, list of current FDI clients, and the qualifications of their expert team. The staff directly handling your files must hold official tax agent licenses, specialized HR certifications, and have extensive practical experience in managing complex legal situations for foreign-invested companies.

4.4. How does the working process and regular coordination work?

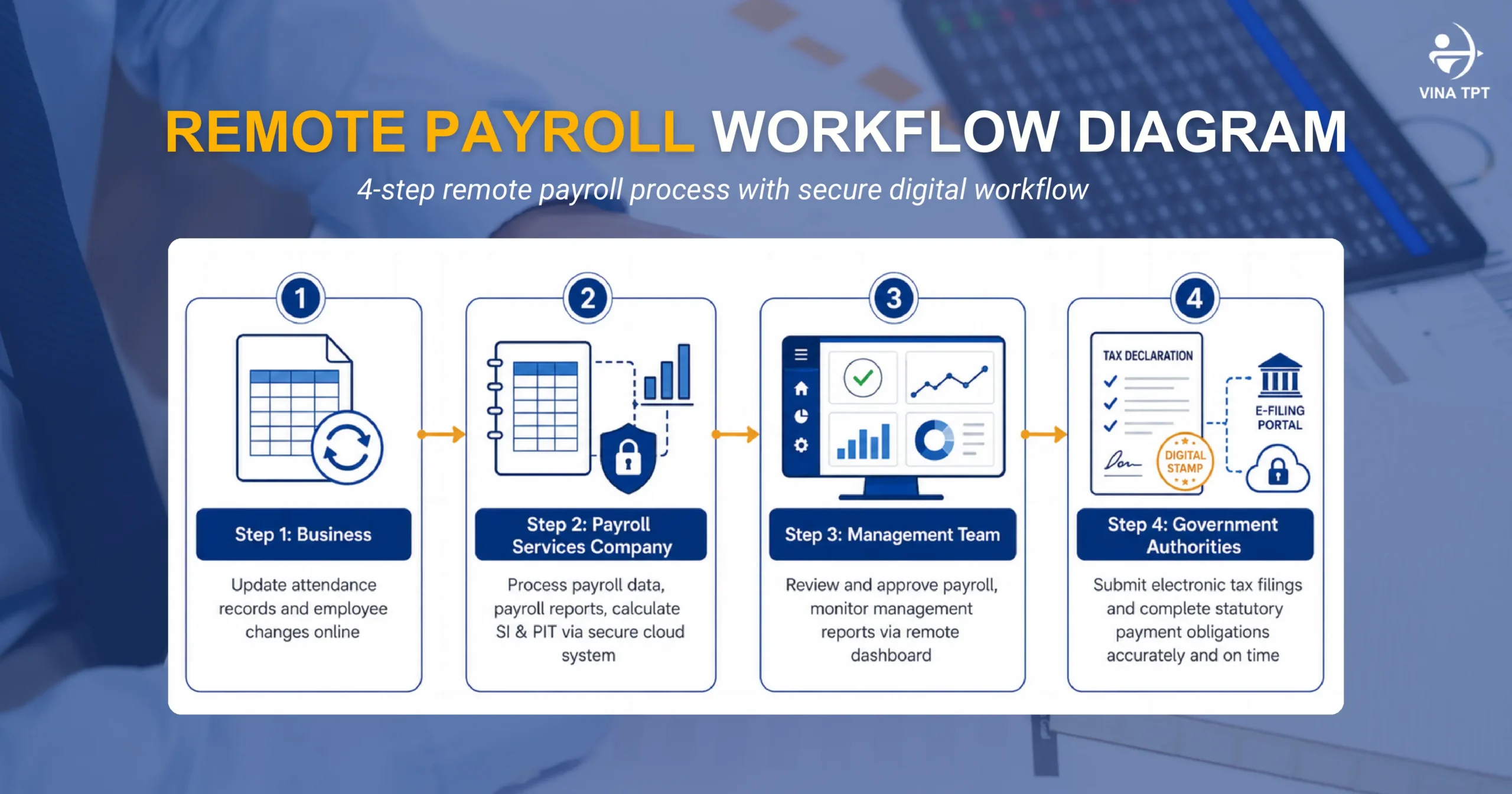

A standardized process typically follows 5 strict steps: (1) Needs assessment and solution consultation; (2) Collection of personnel data and initial attendance records; (3) Parallel run (test payroll) for data reconciliation; (4) Official monthly payroll execution; (5) Periodic reporting and secure payslip distribution to employees.

4.5. What happens if there is an error or incident?

High-quality service providers always sign service contracts with clear Service Level Agreements (SLA) regarding deadlines and accuracy. They are willing to take legal responsibility and compensate for any financial losses (if any) caused by calculation errors or delays on their part, giving customers complete peace of mind.

5. Why Vina TPT is a Trusted Vietnam Payroll Provider

Among the many payroll provider Vietnam options available today, Vina TPT stands out as a trusted partner for FDI companies, thanks to its outstanding competitive advantages (USPs):

- Over 20 years of specialized experience supporting FDI: Vina TPT proudly boasts two decades of hands-on experience, with a deep understanding of foreign management mindsets, corporate culture, and the unique challenges that FDI companies often face when dealing with Vietnamese state authorities.

- Flexible service packages designed for small & medium teams: We understand that every business has its own development path. Vina TPT offers flexible, cost-optimized solutions – from representative offices with just 3–5 employees to companies expanding to hundreds of staff.

- Seamless integration of payroll with full accounting and tax services: This is a major advantage of Vina TPT. By synchronizing salary and insurance data directly with the company’s accounting system and Corporate Income Tax (CIT) declarations, we completely eliminate data discrepancies between HR and accounting departments, while optimizing overall legal costs for the business.

- Bilingual expert team and transparent processes: All account managers at Vina TPT can communicate and work fluently in English, Japanese and have a strong command of finance and HR terminology. Every payroll deadline and tax report is clearly defined in the SLA, ensuring information is always delivered on time and transparently to headquarters.

- Fast response and proactive advisory: Our experts go beyond passive data processing. They actively analyze your company’s HR structure, provide recommendations for optimizing salary scales, bonus policies, and legal cost-saving strategies for insurance and PIT, and respond to any client issues within just a few working hours.

If you are looking for a reliable Vietnam payroll provider, contact Vina TPT today to receive a completely free in-depth consultation from our leading experts and experience a personalized demo tailored to your company’s size and business model.