The period 2025-2026 marks significant developments in Vietnam’s tax and accounting framework. Circular 99/2025/TT-BTC, effective from January 1, 2026, introduces updates to accounting guidance, including changes to the chart of accounts and financial reporting, contributing to Vietnam’s gradual alignment with IFRS standards.

In addition, recent amendments to Corporate Income Tax regulations and the revised Law on Personal Income Tax (effective from July 1, 2026) will have a direct impact on compliance and business operations. Furthermore, the temporary VAT reduction to 8% (subject to government extension policies) continues to affect tax planning and cost structures for businesses.

These changes create challenges for many FDI enterprises in staying compliant, especially when simultaneously handling Vietnamese Accounting Standards (VAS), reconciliation with International Financial Reporting Standards (IFRS), tax management, and payroll for foreign employees (expatriates).

In this context, many companies choose outsourced finance and accounting services as a strategic solution. These services ensure compliance, optimize costs, reduce operational burden, and allow businesses to focus on core activities.

This article provides a comprehensive overview of the 5 key functions you should look for in an outsourced finance and accounting package. It is designed to help foreign investors select a reputable and suitable service provider in Vietnam.

1. Bookkeeping Management

Bookkeeping services (in outsourced finance and accounting package) involve the collection, verification, and recording of all financial transactions according to applicable accounting standards. It forms the foundation for preparing financial statements, tax declarations, and working with auditors.

From 2026 onward, with the implementation of Circular 99/2025/TT-BTC, enterprises must comply with the new chart of accounts and regulations under Vietnamese Accounting Standards (VAS). At the same time, they often need to address differences between VAS (used for local regulatory reporting) and IFRS (required by headquarters or parent companies). Accurate recording from the very beginning is therefore essential.

A professional outsourced finance and accounting package typically includes the following bookkeeping services:

Monthly tasks:

- Collection, verification, and secure storage of valid accounting documents (vouchers)

- Data entry and review of accounts according to the new chart of accounts under Circular 99

- Preparation of detailed monthly financial statements

- Provision of ad-hoc managerial reports upon request

Year-end tasks:

- Preparation of annual financial statements in accordance with VAS

- Close coordination with independent auditors (liaising with auditors)

- Support for VAS–IFRS reconciliation for headquarters reporting

Important note: A common misconception is that simply entering all documents is sufficient. In reality, transactions must be recorded correctly according to Vietnamese accounting principles (VAS). Even small deviations can lead to tax adjustments, prolonged audits, and unnecessary additional costs.

>>> You may also be interested in: Best Bookkeeping Services for Startups in Vietnam

2. Financial Reporting & Management Reports

Financial reporting is crucial not only for regulatory compliance but also as a vital tool for monitoring business performance and supporting timely decision-making.

In an outsourced finance and accounting package, financial reporting services usually include:

- Preparation of monthly and annual financial statements in accordance with Vietnamese accounting standards

- Consolidation of financial statements (where required)

- Delivery of customized management reports, such as cash flow statements, budget variance analysis, KPI tracking, and cost analysis

For FDI companies, receiving timely monthly financial reports is particularly important. These reports enable leadership to closely monitor the company’s financial position and adjust business plans promptly.

3. Tax Compliance & Filing

For foreign-invested enterprises, lack of familiarity with Vietnam’s tax regulations is a frequent cause of errors and penalties. Obligations include Value-Added Tax (VAT), Corporate Income Tax (CIT), Personal Income Tax (PIT), Foreign Contractor Tax (FCT), Withholding Tax (WHT), and specialized reports such as investment activity reports.

A comprehensive Tax Compliance & Filing service within outsourced finance and accounting typically covers:

- Monthly or quarterly VAT declaration and payment

- Provisional CIT declaration and finalization under the Corporate Income Tax Law

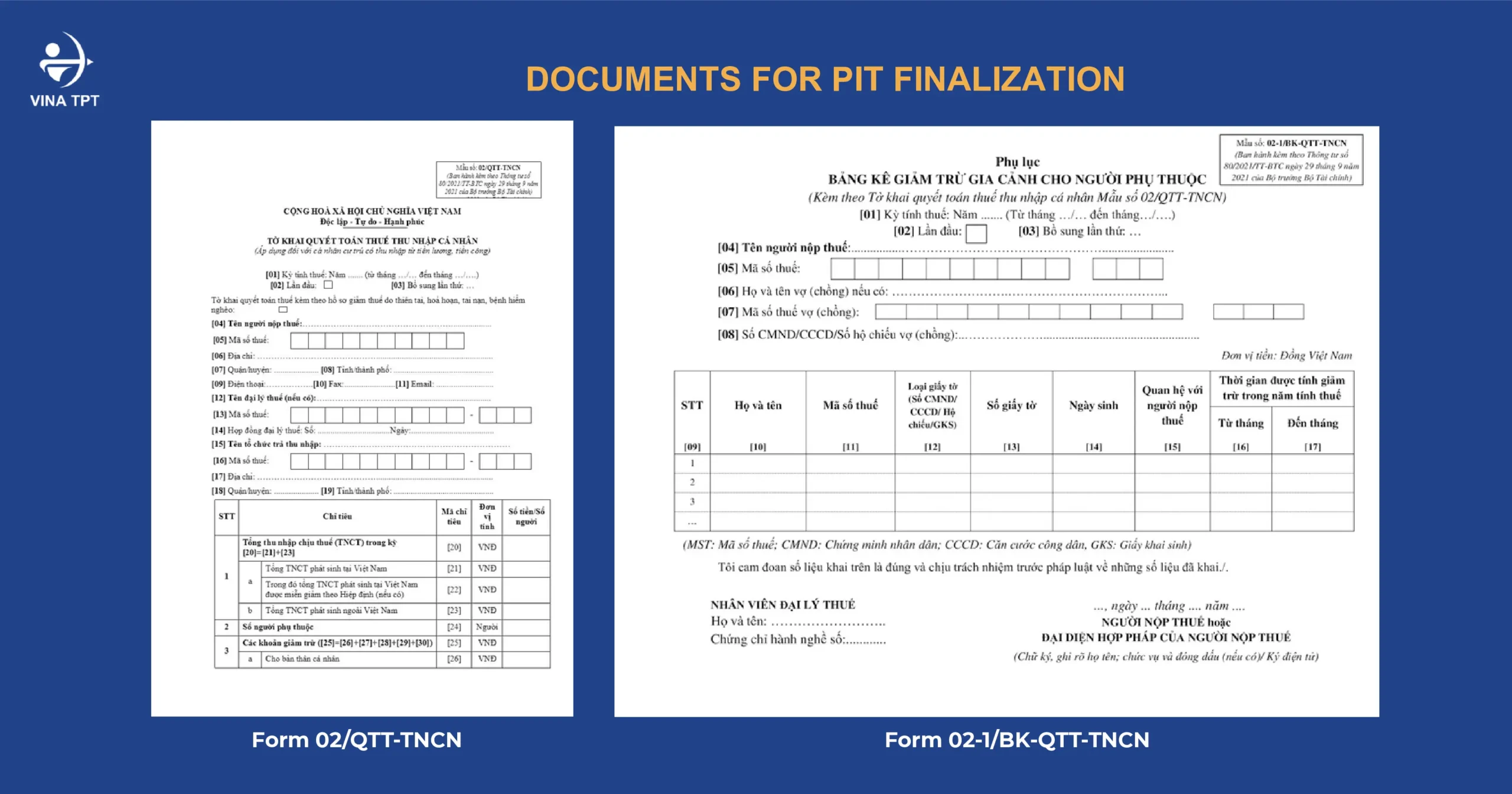

- Monthly, quarterly, and annual PIT declaration and payment according to the new 5-bracket progressive tax schedule effective 2026

- Handling of Foreign Contractor Tax (FCT) and Withholding Tax (WHT)

- Support for VAT refund and transfer pricing documentation

- Preparation of statistical reports and Investment Activity Reports (IAR) specifically required for FDI companies

Non-compliance can result in administrative fines, tax reassessments, late-payment interest, or even temporary suspension of the tax code – all of which directly impact business operations. This is why many FDI enterprises rely on professional tax compliance services to ensure full adherence from the outset.

EXPLORE OUR ACCOUNTING & TAX SERVICES

4. Payroll & Employee Tax Handling

Payroll and employee tax handling involves the calculation of salaries, benefits administration, and management of all tax and insurance obligations related to employees. This is a critical function in business operations, as it directly affects employee welfare and the company’s legal compliance.

A professional outsourced finance and accounting package typically includes the following payroll services:

- Monthly payroll calculation and preparation of confidential payroll reports

- Processing of mandatory social insurance, health insurance, and unemployment insurance contributions in accordance with Vietnamese regulations

- Withholding, declaration, and annual finalization of Personal Income Tax (PIT)

- Specialized support for matters involving foreign employees (expatriates)

Important note for FDI companies: When a company employs expatriates, additional requirements such as visas, work permits, Temporary Residence Cards, and residency-based Personal Income Tax rules must be handled accurately and in coordination with payroll processing. Therefore, it is recommended to choose a outsourced finance and accounting provider that can support these immigration-related requirements alongside payroll services. This helps ensure consistency, optimize costs, and minimize operational risks.

In practice, effective payroll management goes far beyond simply calculating salaries. It encompasses numerous legal and tax obligations that are frequently updated in Vietnam. By outsourcing this function, many FDI enterprises can significantly reduce the workload on their internal HR teams, ensure full regulatory compliance, and maintain workforce stability – even as labor and tax regulations continue to evolve.

>>> You may also be interested in:

- https://vinatpt.com/electronic-employment-contracts-vietnam-decree-337-2025/

- Overview of Vietnam public holidays for Employees in 2026

5. Advisory & Ongoing Support

Outsourced finance and accounting should not be limited to execution. It must also provide proactive, strategic advisory support.

At Vina TPT, we go beyond basic services by offering:

- Legally compliant tax optimization advice

- Guidance on capital structuring and transfer pricing for related-party transactions

- Support during tax audits and liaison with auditors

- Services of a Qualified Chief Accountant (authorized to sign documents and represent the company with state authorities)

- Assistance in setting up accounting systems and internal controls

Many of our FDI clients have successfully avoided major risks thanks to early advice on the Global Minimum Tax and changes under the 2025 CIT Law. We act not only as a service provider but as a long-term strategic partner – supporting your company from initial setup through expansion.

How to build the right outsourced finance package for your FDI company

To choose the most suitable outsourced finance and accounting package, consider the following:

- Scale of transactions, number of employees, and expatriate requirements

- Level of advisory support needed (from basic bookkeeping to full strategic advisory)

When selecting a service provider, FDI enterprises should also evaluate:

-

- Professional expertise and clear workflows that ensure full compliance with Vietnamese Accounting Standards (VAS)

- Responsiveness and team-based support model (rather than reliance on a single individual)

- Risk management capabilities and clear contractual responsibilities

- Strong data confidentiality clauses, including scope of information use, security obligations, and breach remedies

With over 20 years of experience in company establishment consulting and financial services tailored for FDI enterprises, Vina TPT fully meets these criteria. We support clients from the initial structuring and setup phase through ongoing finance and accounting operations after incorporation.

Each client is assigned a dedicated team (Assistant – Senior – Manager levels) for multi-layer review and timely issue resolution. We commit to responding within 24-48 hours, ensuring continuous support throughout your operations in Vietnam.

Contact Vina TPT today for a free consultation and to build the most suitable outsourced finance and accounting package for your business model.