As part of the Vietnam tax policy updates 2025, several new regulations related to Corporate Income Tax (CIT), Value Added Tax (VAT), Personal Income Tax (PIT), and social insurance are scheduled to take effect starting from September 2025. These changes are expected to directly impact financial reporting, payroll processes, and compliance operations across both Vietnamese and FDI enterprises.

To help businesses stay compliant and proactively adjust their internal procedures, this article provides a clear breakdown of the most important regulatory updates you need to be aware of.

In this article, we break down the most important tax regulations businesses need to prepare for in 2025.

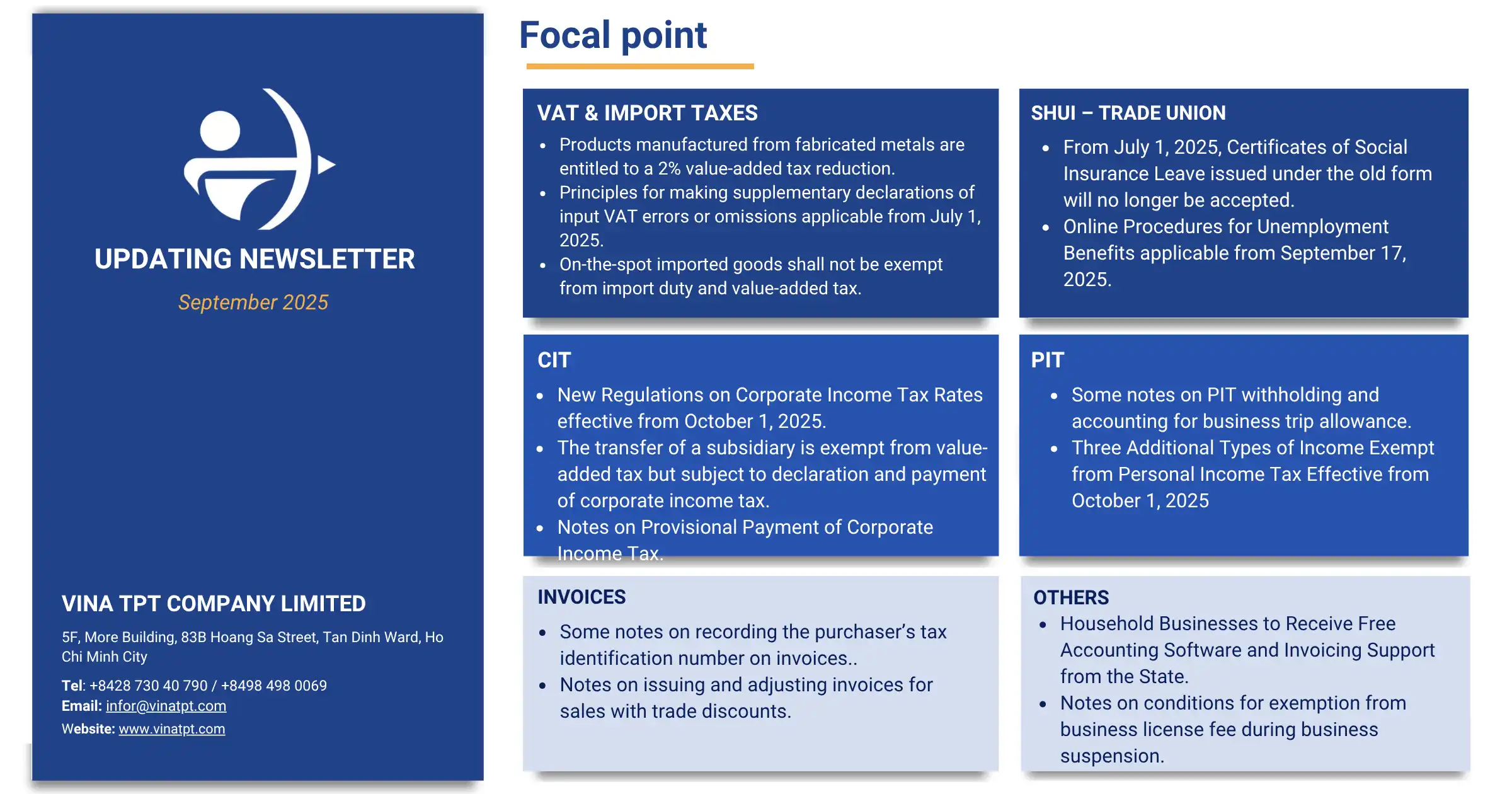

1. Value-Added-Tax & IMPORT TAXES

1.a. Products manufactured from fabricated metals are entitled to a 2% value-added tax reduction.

Official Letter No. 6099/TCS3-QLDN2 dated September 11, 2025 of Dong Nai Tax Department regarding the case where a company manufactures and processes metal products, in which the determination of VAT reduction on sold products is made in accordance with Circular No. 174/2025/TT-BTC, specifically as follows:

- The company shall identify its products based on the product codes, names, and descriptions provided in the Appendix issued together with Decision No. 43/2018/QD-TTg, and compare them with the List of goods and services not eligible for value-added tax (VAT) reduction issued together with Circular No. 174/2025/TT-BTC. In cases where the products fall under the List of goods attached to Circular No. 174/2025/TT-BTC, they shall not be entitled to VAT reduction.

- For products manufactured from fabricated metals classified under Section 25, which are not included in the List of goods and services issued together with Circular No. 174/2025/TT-BTC, a VAT reduction shall apply.

1.b. Principles for making supplementary declarations of input VAT errors or omissions applicable from July 1, 2025.

Official Letter No. 3915/CT-CS dated September 18, 2025 of the Tax Department regarding VAT policies, specifically as follows:

- The Tax Department stated that, from July 1, 2025, the Law on Value-Added Tax No. 48/2024/QH15 and Decree No. 181/2025/ND-CP have specifically provided regulations on the declaration and deduction of input VAT in cases of errors or omissions. Enterprises are therefore requested to study and comply with these provisions. Accordingly, under Point đ, Clause 1, Article 14 of Law No. 48/2024/QH15 and Clauses 5 and 6, Article 23 of Decree No. 181/2025/ND-CP, when errors or omissions in input VAT are detected, business establishments shall make supplementary declarations in accordance with the following principles:

- A supplementary declaration shall be made in the month or quarter in which the error or omission in input VAT arises, if such error or omission results in an increase in tax payable or a reduction in refundable tax for that month or quarter.

- A supplementary declaration shall be made in the month or quarter when the error or omission is detected, if such error or omission results in a decrease in tax payable, or only increases or decreases the amount of VAT to be carried forward to the subsequent period.

1.c. On-the-spot imported goods shall not be exempt from import duty and value-added tax.

Official Letter No. 22303/CHQ-GSQL dated September 5, 2025 of the Customs Department regarding on-the-spot imported goods, specifically as follows:

- Clause 3 Article 3 of Law No. 90/2025/QH15 supplements Article 47a of the Customs Law, stipulating that on-the-spot import and export goods are goods delivered and received in Viet Nam under the designation of a foreign trader pursuant to sale, processing, leasing, or borrowing contracts. Cases that meet these conditions shall carry out customs procedures under Article 35 of Circular No. 08/2015/TT-BTC (as amended by Circular No. 167/2025/TT-BTC) and Article 86 of Circular No. 38/2015/TT-BTC (as amended by Circular No. 39/2018/TT-BTC).

- According to Circular No. 134/2016/TT-BTC (as amended by Circular No. 18/2021/TT-BTC), in cases where on-the-spot imports are not registered under the processing type, the importer must declare and pay import duty based on the applicable duty rate and customs value at the time of registration. If import duty has been paid for production or business purposes and the imported products have been actually exported abroad or to a non-tariff zone, the paid duty shall be refunded in accordance with Article 36 of this Circular

- On-the-spot import and export goods remain subject to VAT. Where goods are registered under other types (not processing), the taxpayer shall use code A11 (commercial import) or A12 (import for production and business) to declare and pay import duty and VAT.

2. Personal Income Tax (PIT)

2a. Some notes on PIT withholding and accounting for business trip allowance.

Official Letter No. 2284/CTH-QLDN1 dated September 15, 2025 of the Can Tho City Tax Department regarding taxable personal income (PIT) on business trip allowances, specifically as follows:

- Taxable PIT income with respect to lump-sum business trip allowances: This is the portion of business trip allowances exceeding the limits prescribed by the State. Specifically: For employees working in business organizations and representative offices, the limit on business trip allowances shall be applied consistently with the level determined for corporate income tax (CIT) purposes. For employees working in international organizations or representative offices of foreign organizations, the limit on business trip allowances shall be applied in accordance with the regulations of such international organizations or representative offices of foreign organizations (see Point đ.4, Clause 2, Article 2 of Circular No. 111/2013/TT-BTC).

Travel expenses and accommodation costs for employees on business trips shall be deductible if supported by sufficient invoices and documents.

- Where the enterprise has a financial/internal regulation stipulating allowances for travel, accommodation, and per diem for employees on business trips, and such regulation is properly implemented, these expenses shall be deductible.

- Payment by employees’ personal bank cards for business trip expenses of VND 20 million or more (including airfares):

- Such expenses shall be deductible if the following conditions are met:

- Valid invoices and supporting documents are available.

- A decision or written authorization for the employee’s business trip is issued.

- The enterprise’s financial/internal regulation permits employees to pay using personal bank cards, with subsequent reimbursement by the enterprise.

- Purchase of air tickets via e-commerce websites: The documents serving as the basis for deductibility include the electronic air ticket, boarding pass, and the enterprise’s non-cash payment vouchers showing the individual undertaking the transportation service.

Explore Tax Services in Viet Nam

2b. Three Additional Types of Income Exempt from Personal Income Tax Effective from October 1, 2025

According to the new provisions in the Law on Science, Technology and Innovation 2025 (No. 93/2025/QH15), effective from October 1, 2025, Clause 3, Article 71 of this Law supplements Points 18, 19, and 20 after Point 17 of Article 4 on tax-exempt income under the Law on Personal Income Tax 2007, as amended and supplemented.

Accordingly, from October 1, 2025, three additional types of income will be exempt from Personal Income Tax (PIT), including:

- Income from salaries and wages received from performing science, technology, and innovation tasks.

- Income from copyright related to science, technology, and innovation tasks when the results of such tasks are commercialized in accordance with the laws on science, technology, innovation, and intellectual property.

- Income of individual investors and experts working for start-up innovation projects, founders of start-up enterprises, and individual investors contributing capital to venture capital funds.

3. Corporate Income Tax (CIT)

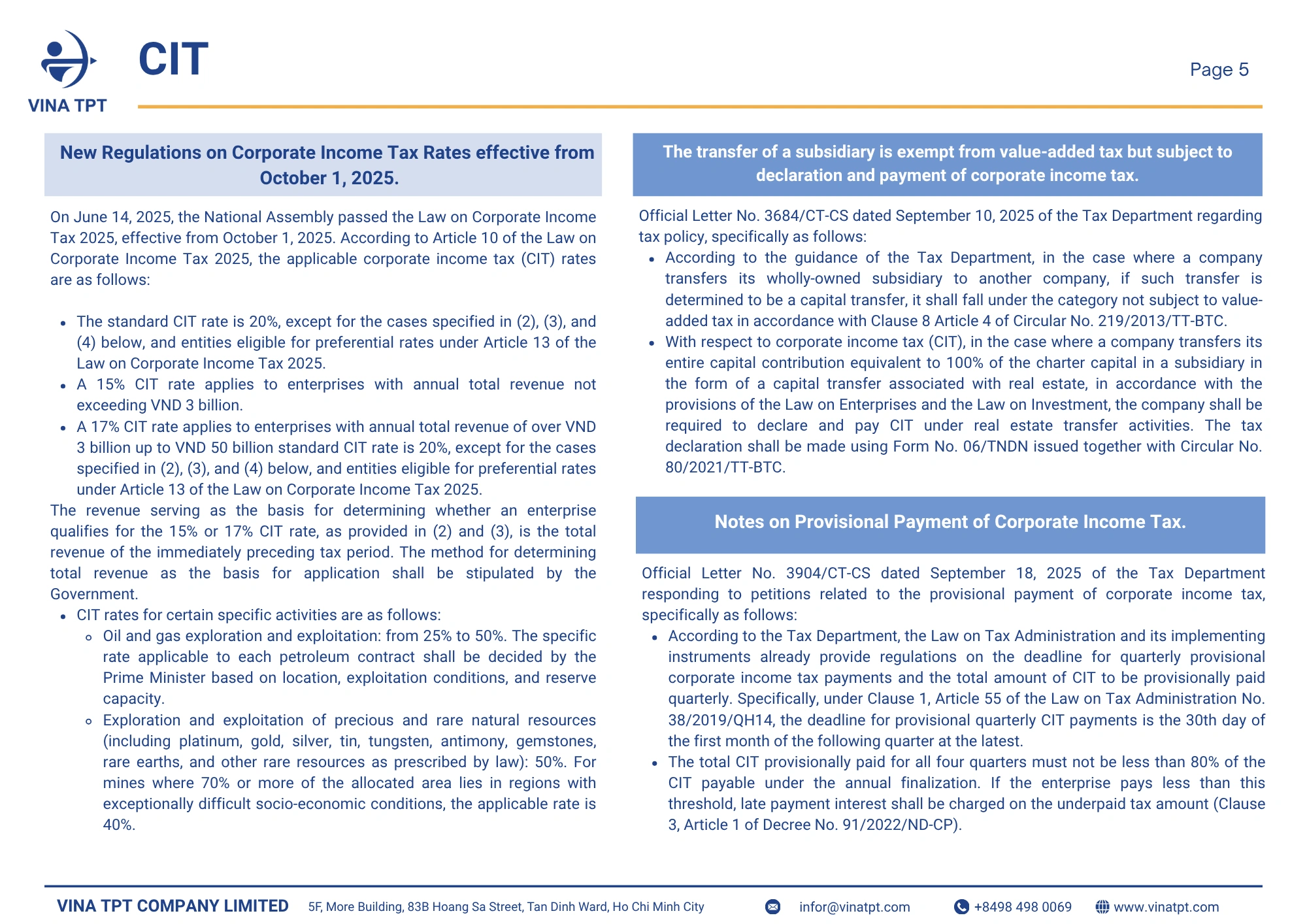

3a. New Regulations on Corporate Income Tax Rates effective from October 1, 2025.

On June 14, 2025, the National Assembly passed the Law on Corporate Income Tax 2025, effective from October 1, 2025. According to Article 10 of the Law on Corporate Income Tax 2025, the applicable corporate income tax (CIT) rates are as follows:

- The standard CIT rate is 20%, except for the cases specified in (2), (3), and (4) below, and entities eligible for preferential rates under Article 13 of the Law on Corporate Income Tax 2025.

- A 15% CIT rate applies to enterprises with annual total revenue not exceeding VND 3 billion.

- A 17% CIT rate applies to enterprises with annual total revenue of over VND 3 billion up to VND 50 billion standard CIT rate is 20%, except for the cases specified in (2), (3), and (4) below, and entities eligible for preferential rates under Article 13 of the Law on Corporate Income Tax 2025

The revenue serving as the basis for determining whether an enterprise qualifies for the 15% or 17% CIT rate, as provided in (2) and (3), is the total revenue of the immediately preceding tax period. The method for determining total revenue as the basis for application shall be stipulated by the Government.

CIT rates for certain specific activities are as follows:

- Oil and gas exploration and exploitation: from 25% to 50%. The specific rate applicable to each petroleum contract shall be decided by the Prime Minister based on location, exploitation conditions, and reserve capacity.

- Exploration and exploitation of precious and rare natural resources (including platinum, gold, silver, tin, tungsten, antimony, gemstones, rare earths, and other rare resources as prescribed by law): 50%. For mines where 70% or more of the allocated area lies in regions with exceptionally difficult socio-economic conditions, the applicable rate is 40%.

3b. The transfer of a subsidiary is exempt from value-added tax but subject to declaration and payment of corporate income tax.

Official Letter No. 3684/CT-CS dated September 10, 2025 of the Tax Department regarding tax policy, specifically as follows:

- According to the guidance of the Tax Department, in the case where a company transfers its wholly-owned subsidiary to another company, if such transfer is determined to be a capital transfer, it shall fall under the category not subject to value-added tax in accordance with Clause 8 Article 4 of Circular No. 219/2013/TT-BTC.

- With respect to corporate income tax (CIT), in the case where a company transfers its entire capital contribution equivalent to 100% of the charter capital in a subsidiary in the form of a capital transfer associated with real estate, in accordance with the provisions of the Law on Enterprises and the Law on Investment, the company shall be required to declare and pay CIT under real estate transfer activities. The tax declaration shall be made using Form No. 06/TNDN issued together with Circular No. 80/2021/TT-BTC.

3c. Notes on Provisional Payment of Corporate Income Tax.

Official Letter No. 3904/CT-CS dated September 18, 2025 of the Tax Department responding to petitions related to the provisional payment of corporate income tax, specifically as follows:

- According to the Tax Department, the Law on Tax Administration and its implementing instruments already provide regulations on the deadline for quarterly provisional corporate income tax payments and the total amount of CIT to be provisionally paid quarterly. Specifically, under Clause 1, Article 55 of the Law on Tax Administration No. 38/2019/QH14, the deadline for provisional quarterly CIT payments is the 30th day of the first month of the following quarter at the latest.

- The total CIT provisionally paid for all four quarters must not be less than 80% of the CIT payable under the annual finalization. If the enterprise pays less than this threshold, late payment interest shall be charged on the underpaid tax amount (Clause 3, Article 1 of Decree No. 91/2022/ND-CP).

4. Social Insurance – Trade Union

a. From July 1, 2025, Certificates of Social Insurance Leave issued under the old form will no longer be accepted.

Official Letter No. 5761/BYT-KCB dated August 27, 2025 of the Ministry of Health regarding the settlement of difficulties in implementing social insurance regimes for employees, specifically as follows:

- Accordingly, the Ministry of Health notes that Certificates of Social Insurance Leave issued prior to the effective date of Circular No. 25/2025/TT-BYT (July 1, 2025) shall remain valid as the basis for entitlement to social insurance benefits. For Certificates issued after July 1, 2025, it is mandatory to use the new form promulgated under Circular No. 25/2025/TT-BYT. The difference between the new form and the old form (issued under Circular No. 18/2022/TT-BYT) lies in the addition of information on the employee’s citizen identification number/identity card number/passport number/personal identification number; other contents remain unchanged from the old form.

- During the initial implementation of Circular No. 25/2025/TT-BYT, for documents issued by hospitals still using the old form and not yet switched to the new form, in order to ensure employees’ rights and avoid inconvenience, the Ministry of Health has requested that enterprises prepare a list of employees whose documents were issued by hospitals in non-compliance with regulations, and submit an official letter to the Department of Health or the health authority of the relevant ministries/agencies managing such hospitals, requesting the supplementation of information on the documents already issued, as prescribed in Point b, Clause 4, Article 28 of Circular No. 25/2025/TT-BYT.

As for Certificates of Social Insurance Leave without the hospital’s seal due to the seal not yet being updated to the new address following a merger, the Ministry of Health has stated that, under Clause 8, Article 69 of Decree No. 188/2025/ND-CP, medical examination and treatment establishments are permitted to continue using their old seals until new seals are issued.

b. Online Procedures for Unemployment Benefits applicable from September 17, 2025.

Decision No. 1295/QD-TTPVHCC dated September 17, 2025 of the People’s Committee of Hanoi City announcing the List of administrative procedures on unemployment insurance to be piloted on the National Public Service Portal under the management competence of the Department of Home Affairs of Hanoi City, specifically as follows:

This Decision announces six procedures concerning the entitlement to and termination of unemployment benefits to be piloted by the Hanoi Department of Home Affairs on the National Public Service Portal as from September 17, 2025, including:

- Settlement of entitlement to unemployment benefits

- Monthly notification of job search activities.

- Settlement of entitlement to unemployment benefits

- Settlement of entitlement to unemployment benefits

- Transfer of entitlement to unemployment benefits (integrated procedure for transfer-out and transfer-in).

- Termination of entitlement to unemployment benefits.

This Decision takes effect from the date of signing.

5. OTHER

a. Household Businesses to Receive Free Accounting Software and Invoicing Support from the State.

Official Letter No. 3914/CT-CS dated September 18, 2025 of the Tax Department regarding the response to the petition of the Vietnam Banks Association:

- With respect to the use of invoices by household businesses, the Tax Department notes that, pursuant to the provisions of Decree No. 70/2025/NĐ-CP, from June 1, 2025, when selling goods or providing services directly to consumers, household businesses under the lump-sum tax regime with annual revenue exceeding VND 1 billion must issue electronic invoices generated from cash registers connected to and transmitting data to the tax authority, and deliver such invoices to buyers. The electronic invoice data is already available on the tax authority’s system, allowing both sellers and buyers to look up invoices on the system without the need to print paper copies.

- Under the current guidance provided in Circular No. 40/2021/TT-BTC, there is no provision requiring lump-sum household businesses to retain purchase invoices or supporting documents.

- As stipulated at Point b, Clause 4, Article 13 of Circular No. 40/2021/TT-BTC, in cases where a lump-sum household business changes its business scale (premises size, labor use, or revenue), it must declare adjustments and supplements to the Tax Return using Form No. 01/CNKD. The tax authority, based on the household business’s tax return and the tax sector’s database, shall issue a Notice of adjustment of lump-sum tax if it determines that declared revenue has changed by 50% or more compared to the previously assessed lump-sum revenue, effective from the time of such change within the tax year.

Furthermore, pursuant to Clause 3, Article 12 of Resolution

No. 198/2025/QH15, the State shall allocate funding to provide free shared digital platforms and accounting software for small and micro enterprises, household businesses, and individual business households. At present, the Ministry of Finance is drafting a Decree guiding the implementation of this Resolution, which will include provisions on the measures to support the free provision of shared digital platforms and accounting software for small and micro enterprises, household businesses, and individual businesses.

b. Notes on conditions for exemption from business license fee during business suspension.

Official Letter No. 1355/QNG-QLDN1 dated September 4, 2025, of the Quang Ngai Provincial Tax Department on guidance regarding business license fees

- The conditions for exemption from the business license fee during business suspension are stipulated in Clause 2, Article 1 of Decree No. 22/2020/NĐ-CP and Clause 4, Article 1 of Circular No. 65/2020/TT-BTC, as follows: a written request for suspension of production and business operations must be submitted to the tax authority or the business registration authority before the deadline for payment of the business license fee (January 30 each year), and the business license fee of the year in which suspension is requested has not yet been paid.

- Accordingly, if a Company has submitted a written request to the business registration authority to suspend production and business operations in the calendar year 2025 (from January 1 to December 31) before the license fee payment deadline (before January 30) and has not yet paid the 2025 business license fee, then the Company is not required to pay the license fee for 2025.

However, if the above conditions are not satisfied, the Company must pay the business license fee for 2025.

6. INVOICES

a. Some notes on recording the purchaser’s tax identification number on invoices.

Official Letter No. 3955/CT-CS dated September 19, 2025 of the Tax Department regarding e-invoices, specifically as follows:

- The presentation of the buyer’s name, address, and taxpayer identification number on e-invoices shall comply with the provisions of Clause 5 and Point c, Clause 14, Article 10 of Decree No. 123/2020/ND-CP (as amended and supplemented at Points a and d, Clause 7, Article 1 of Decree No. 70/2025/ND-CP). Accordingly, in cases where the buyer is a business establishment with a TIN, the buyer’s name, address, and TIN stated on the invoice must be consistent with the information on the enterprise/branch registration certificate, household business registration certificate, tax registration certificate, or TIN notification

- If the purchaser does not have a tax identification number, the TIN is not required to be shown on the e-invoice. In addition, in cases specified at Point c, Clause 14 , Article 10, it is not mandatory to indicate the purchaser’s name, address, or TIN on the invoice. As from June 1, 2025, where the purchaser provides a TIN or personal identification number, the invoice must also include such TIN or personal identification number.

- For e-invoices generated from cash registers, the invoice must show the purchaser’s name, address, tax identification number/personal identification number/telephone number if so requested by the purchaser (see Clause 3, Article 11 of Decree No. 123/2020/ND-CP, as amended and supplemented under Clause 8, Article 1 of Decree No. 70/2025/ND-CP).

b. Notes on issuing and adjusting invoices for sales with trade discounts.

Official Letter No. 1802/CTH-QLDN3 dated September 3, 2025, of the Can Tho City Tax Department regarding trade discount invoices, specifically as follows:

In this document, the Can Tho City Tax Department provided guidance on determining VAT taxable prices in cases of trade discounts, how to present discount amounts on invoices, and how to handle adjustment invoices when discounts are based on quantity or sales volume. Specifically:

VAT taxable price: The VAT taxable price is the selling price after deducting the trade discount given to customers, excluding VAT (Clause 2, Article 14 of Decree No. 181/2025/NĐ-CP).

Presentation on invoices: The invoice must clearly indicate the trade discount amount (Point đ, Clause 6, Article 10 of Decree No. 123/2020/NĐ-CP.

Discounts based on quantity or sales volume:

- Adjustment on the last purchase/next period invoice: The discount amount shall be adjusted on the sales/service invoice of the last purchase or subsequent period, ensuring the discount amount does not exceed the value of goods or services recorded on that invoice.

- Issuing an adjustment invoice: An adjustment invoice may be issued together with a list of the invoices subject to adjustment, including amounts and tax adjustments. The list must be kept at the entity and presented upon request by the tax authority or other competent state authority (Clause 13, Article 1 of Decree No. 70/2025/NĐ-CP amending and supplementing Article 19 of Decree No. 123/2020/NĐ-CP.

- Tax return adjustments: Based on the adjustment invoice and related records, both the buyer and the seller shall declare adjustments to sales revenue, purchase revenue, input and output VAT in the period when the adjustment invoice is issued.

- Adjustment invoice for trade discounts: This is an adjustment invoice for previously issued invoices, used to adjust differences in amounts only; it is not used to declare sales revenue already incurred. Accordingly, in the electronic invoice system of the General Department of Taxation, the line “Total amount before tax” will display the trade discount amount, while the line “Total trade discount amount” will display as 0.

Contact us for support

📞 (+84) 984 980 069

📧 infor@vinatpt.com

🌐www.vinatpt.com

🏢 5th Floor, More Building, 83B Hoang Sa, Tan Dinh Ward, Ho Chi Minh City